Wanna know the kind of impulse buying checklist that doesn’t make you feel like a reckless child in a candy store, but like a boss in control of your own money? This post is dedicated to showing you how to flip the script on overspending, without all the shame and guilt that usually keeps you stuck.

You know the sting: that rush of excitement at checkout, followed by the sinking weight in your stomach when the credit card bill shows up. It feels like you betrayed yourself yet again. But pause & analyze the situation; you’re not broken. You’re a normal, decent, feeling human being in a consumer culture that’s built to trip you every step of the way.

What you’re going to learn is how to dismantle those impulses and turn them into strategic decisions with four powerful questions. Instead of white-knuckling your way through temptation, you’ll develop clear-headed rationality to separate true needs from quick dopamine chases.

After you have learned to ask these questions, you will be able to spend with purpose, align purchases with your bigger goals, and even make guilt-free room for pleasure. The end result? Kick-ass confidence in your financial decisions, and freedom from the self-doubt roundabout that’s been draining your energy.

This post is all about building your impulse buying checklist, so you can rebel against staying small and start living your life full-on.

Impulse Buying Checklist

An impulse buying checklist isn’t about punishing yourself for every misstep. When you observe the pattern more deeply, it’s way more about dismantling shame than clipping coupons.

People confuse doing something bad with being bad, which leaves you swimming in self-blame instead of solutions. Consumer culture thrives on your self-doubt, using ads, scarcity tricks, and dopamine spikes to make you trip. Once you restore your innocence and shift focus to strategy, you don’t just curb spending; but reclaim your power.

You see that impulse buying isn’t proof of your weakness but evidence of an environment designed to keep you small. Refusing to half-ass life means setting up systems that serve your growth, not sabotage it. That’s where this checklist comes in: it’s a tool of rebellion, turning impulsivity into a stepping stone toward your actual goals.

Question #1: Does It Actually Solve A Problem Or Irritation In Your Life?

Sorry for not sugarcoating, but I always prefer brutal honesty: a huge chunk of what you label as needs are just dopamine-chasing wants. If the only reason you’re clicking ‘Buy Now’ is that it looks fun or feels like a pick-me-up, then it’s not solving a real problem. That doesn’t make you weak; it makes you human, living in a system designed to exploit your natural urges.

But what it truly is about is separating true problem-solvers from temporary band-aids. Buying groceries for the week? That’s a solution. Grabbing a new gadget because you’re bored? That’s pleasure disguised as necessity. Neither is morally wrong, but the distinction is where your strategy begins.

RELATED POST:

Impulse Buying: Why Your Shame Spiral Is the Real Enemy (And You Should CARE, Instead Of PUNISH)

This is also where rewards come in. Counterintuitively, labeling something as ‘just a reward’ can actually free you. Rewards aren’t bad; they just need to be aligned with self-control, like with the Dopamine Dosing Discipline. When you treat them as rewards rather than necessities, you not only protect your financial flow but you also learn to enjoy them guilt-free.

Pause & analyze the situation: is this purchase about making your life run smoother, or is it about soothing an emotional itch? If it’s the latter, you’re not bad. You just need to admit that it’s a reward, and then move to the next question to see if that reward is worth it right now. That clarity alone keeps you from self-sabotage.

Question #2: Can You Afford It? And Are You Sure About It?

This one sounds obvious, but contrary to popular belief, most impulse buyers have no clue about the real state of their finances. That ignorance isn’t laziness; it’s cultural. You weren’t trained to track your money like a pro, so why would you magically know how to handle it now? Excuse me being blunt, but if you keep avoiding your numbers, you’ll also keep feeling powerless.

Instead, flip it. Knowledge is your strongest thinking partner here. If you know your income, your bills, and what’s left, you’ll have a clear-headed rationality when standing in front of temptation. Can you afford that new jacket without sacrificing rent, groceries, or your bigger dreams? If not, then you’ve got your answer. If yes, then too!

And let me tell ya, there’s a sneaky thrill in proving to yourself that you actually do know your money. It transforms the question from ‘Can I afford this?’ into ‘Am I willing to trade my bigger vision for this quick hit?’ Once you start framing purchases like that, impulse loses half its power.

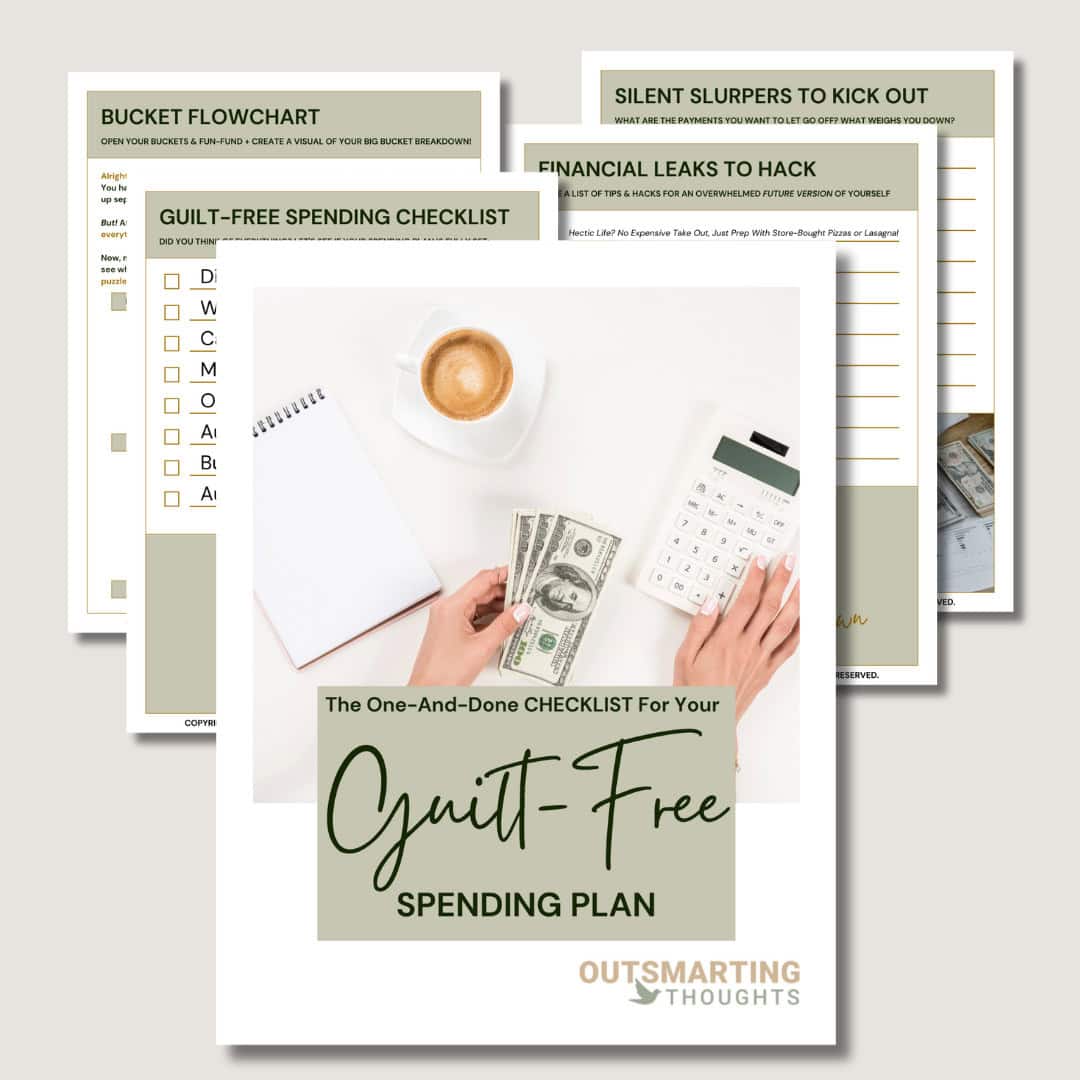

Owning a cashflow strategy is a skill that’ll give you some serious advantages in life. I think budgeting is an aligned action with taking life seriously, and I seriously believe life will reward you for it. If you’re not into high-maintenance strategies like ‘tracking your spending’ and just want to sit down ONCE to direct your financial future, our Guilt-Free Spending Plan Printable is the right cashflow strategy for you! Don’t let anybody outsmart you out of your own money and start budgeting today by simply filling out the form below:

Want a free

ONE-AND-DONE CHECKLIST for aGUILT-FREE SPENDING PLAN? Free up your bandwidth and stop overthinking with this

FREE One-And-Done Checklist for your Guilt-Free Spending Plan!

Simply fill out the form below to get this strategy

delivered straight to your inbox!

Question #3: Is There Another Way To Get What You Want?

Impulse buying thrives on tunnel vision. You see one shiny solution and your brain locks onto it as the only fix. But counterintuitively, there are usually five other ways to solve the same problem; often for free, or at least for less.

What I would like you to consider is this: every purchase has an opportunity cost. Buying new gym gear because you think it’ll motivate you? Maybe what you really need is accountability, not sneakers. Picking up the latest productivity app? You could hack the same system with free tools. The point isn’t to shame you, but to crack open the blinders impulse puts on your mind. The more you try to end financial denial, the better your situation gets.

RELATED POST:

How To Pull Yourself Out Of Financial Denial: An Overachiever’s Strategy To Get Back In Control

Pause & analyze the situation: could borrowing, trading, repurposing, or waiting accomplish the same goal? Sometimes the alternative doesn’t just save money, it works better because it aligns with what you already own and value. When you train your brain to explore alternatives before swiping your card, you stop being a consumer puppet and start being a strategist of your own life.

Question #4: Is Something You Can Do To Counterweight The Expense?

The mistake people make is treating every purchase as a one-way leak. But what it truly is about is building a flow where inflow and outflow dance together. That means whenever you buy, you ask: how can I balance this?

For instance. Sell a pair of jeans if you’re buying another pair. Cancel a subscription you never use if you’re adding a new one. If you’re splurging on dinner, maybe you cook at home the next two nights. This isn’t punishment; it’s just a smart compensation strategy. You’re creating space for your rewards without sinking your bigger ship.

And let’s not sugarcoat it: counterweighting is a rebellious move. Consumer culture doesn’t want you to think about offsets; it wants you to keep stacking clutter. But when you set up this trade-off mindset, you become untouchable. You’re not denying yourself; you’re refusing to half-ass life by letting money leak into things that don’t resonate & align with you.

The secret power here? Counterweighting doesn’t just protect your wallet; it builds trust with yourself. Each trade-off proves you can indulge without spiraling, which rewires your brain to see pleasure as part of your growth, not a threat to it.

Impulse Buying Checklist (Summary)

An impulse buying checklist goes way deeper than just ‘don’t spend.’ It’s about restoring innocence by breaking the false link between doing something bad and being bad. Once you see that overspending is the result of cultural manipulation, not personal defect, you stop swimming in guilt and start swimming toward growth.

The tools from this post give you a clear four-question framework: ask if the purchase solves a problem, check if you can afford it, look for alternatives, and counterweight the expense. This isn’t about deprivation. It’s about shifting from consumer autopilot into intentional rebellion that frees your time, energy, and money for what resonates & aligns with you.

Imagine your future self; calm, strategic, no longer hijacked by impulse. Purchases feel like conscious choices instead of emotional leaks. Your money becomes a partner in building a life you actually want to wake up for.

I wish you the absolute best; consider this your loving shove forward to go kick some ass and start rebelling against the half-ass life today.

This post was all about building your impulse buying checklist, so you can rebel against staying small and start living your life full-on.

We aim to help you out as much as possible, but please keep in mind that the content is only for general informational and educational purposes. We offer our services based on independent research and life-experience only, and so our strategies can never serve as a substitute for professional advice. Trust me, we do not have 'everything figured out', are all still huge works in progress, but hey, what works for us, might work for you too! This is allll up for you to decide... It might not work for you, and that's okay, so cherrypick the stuff that resonates and leave the stuff that doesn't, and let's go!