Wanna know why impulse spending keeps being treated like a moral failure, when in reality it’s a setup designed by consumer culture? This post is dedicated to tearing down the myth that impulse spending is about your lack of discipline, and showing you how the system rigs the game against you.

Let’s not sugarcoat it: you’ve felt the guilt, the shame, and the sting of your own judgment deeply. You hit ‘buy now,’ then spend the rest of the night spiraling in self-blame. But here’s what I’d like you to consider: you’re a normal, decent, feeling human being living in a culture built to tempt you into tripping at every corner. And if you’re an overachiever or overthinker, that cycle of blaming yourself hits even harder, because you hold yourself to impossible standards.

What you’re going to learn is how impulse spending has nothing to do with your worth, and everything to do with the environment you’ve been thrown into. You’ll also see how to ditch the scapegoating, build clear-headed rationality about money, and create a strategy that actually matches your personality.

After you have learned to untangle your self-worth from your shopping patterns, you’ll feel powerful enough to rebel against staying small for mass marketing masterminds. You’ll align your money with goals that truly resonate with you, and that kick-ass confidence will spill over into every other area of your life.

This post is all about impulse spending, so you can stop scapegoating yourself and start reclaiming your future.

Impulse Spending

Impulse spending is misunderstood at its core. People confuse doing something bad with being a bad person, and that mix-up keeps you stuck in a toxic loop. The culture around you thrives on that mistake, because as long as you think you’re the problem, you’ll keep trying to ‘fix yourself’, let’s face it, with another purchase or quick-fix trend.

But here, you can pause & analyze the situation; because impulse spending really is not a character flaw. It’s a misaligned action in a culture that constantly waves shiny objects in your face. You’re not broken for slipping up. The only thing broken is the system profiting off your self-doubt roundabout.

Once you restore your innocence, believe in your capacity, and put the right goals and strategy in place, the whole game changes. Instead of drowning in guilt, you’ll start using your money as a tool to level up and create the life you refuse to half-ass.

The Financial Denial Trap & A Rigged Consumer System

Financial denial is one of the biggest traps you’ll ever face. It’s the pattern of ignoring what’s really happening in your bank account because facing it feels unbearable. And let me tell ya, that silence doesn’t come from laziness. It comes from a culture that conditions you to escape into shopping instead of equipping you with financial literacy.

RELATED POST:

How To Pull Yourself Out Of Financial Denial: An Overachiever’s Strategy To Get Back In Control

Contrary to popular belief, impulse spending doesn’t come from a moral weakness. It comes from being bombarded with ads, limited-time deals, and dopamine hooks designed to make you cave. When you observe the pattern more deeply, it’s way more about a consumer system engineered to keep you small, ashamed, and endlessly buying.

If you’re stuck in financial denial, you’re not failing. You’re surviving a setup. The guilt you feel after impulse spending? That’s not your conscience warning you; it’s the residue of marketing manipulation mixed with shame culture. The industry wants you distracted, so you don’t notice how much power you’d gain by rebelling against their game.

Stop confusing a rigged system with your own character. Recognize the denial, but don’t punish yourself for it. Instead, use it as proof that you’re normal in an abnormal environment. That awareness becomes your first step toward regaining control, not by being ‘better,’ but by choosing not to play by rules designed to make you lose.

If Nobody Taught You, How Can It Be A Character Flaw?

Excuse me being a bit confrontational, but can you feel how MEAN this expectation is? How on Earth can impulse spending be seen as a character flaw if nobody actually teaches financial literacy? You went through school memorizing algebra formulas, but probably never learned how to budget, plan, or calculate the cost of your own bucket list dreams.

And yet, at the same time, financial literacy isn’t rocket science. At its core, it’s just clear-headed rationality: knowing what you WANT your life to look like, understanding the price tag of those goals, and setting up a budget strategy that fits your personality. For instance. Control freaks like me thrive when tracking every expense, while more laid-back people need a one-and-done system they barely have to touch. Both are valid. Both are strategic. But neither has anything to do with moral worth.

You shouldn’t blame yourself for gaps that society left you with. What you do get to do is pick up the tools now, take the responsibility to fix it, and rebel against staying financially powerless. Because you CAN start aligning your money with the life you want to live.

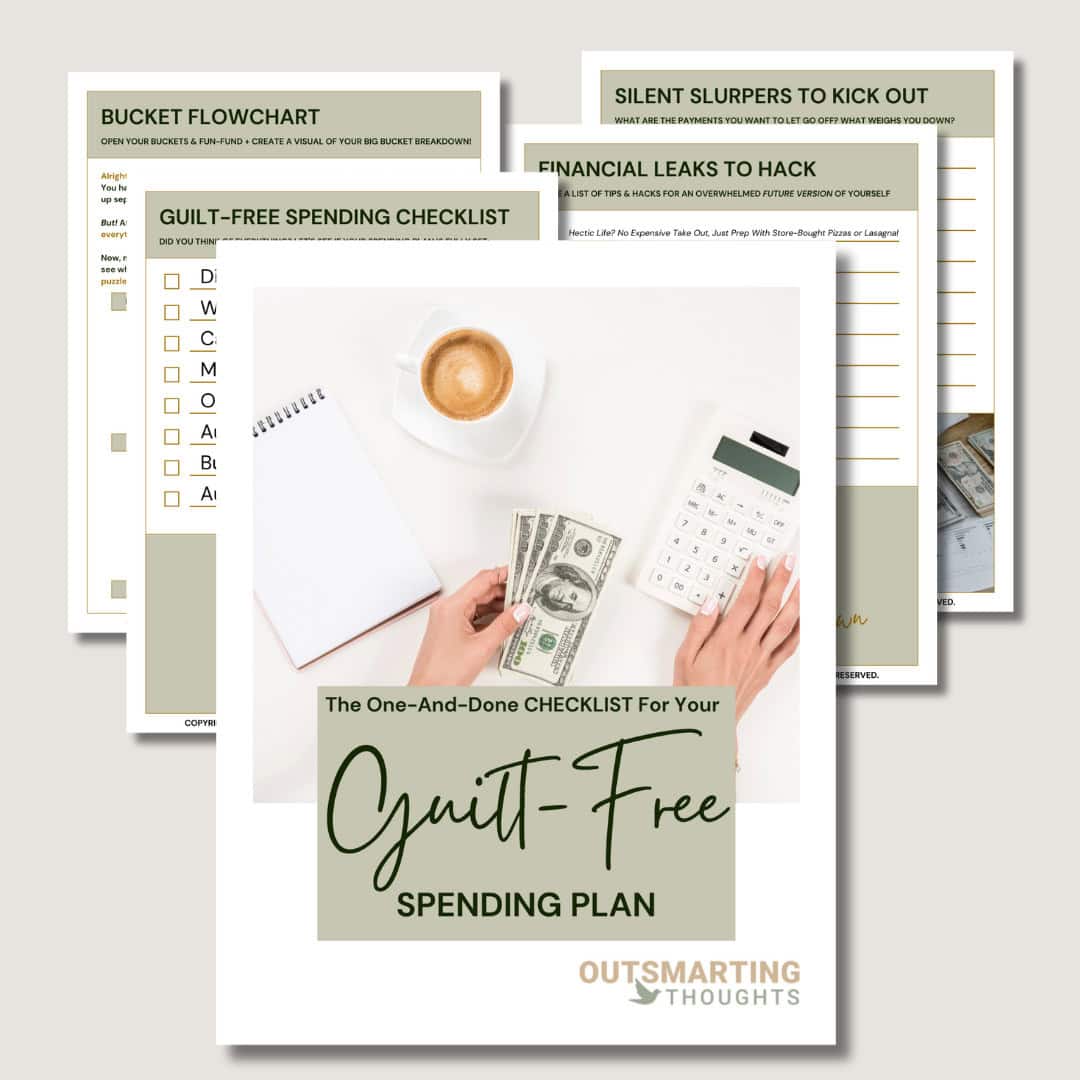

Owning a cashflow strategy is a skill that’ll give you some serious advantages in life. I think budgeting is an aligned action with taking life seriously, and I seriously believe life will reward you for it. If you’re not into high-maintenance strategies like ‘tracking your spending’ and just want to sit down ONCE to direct your financial future, our Guilt-Free Spending Plan Printable is the right cashflow strategy for you! Don’t let anybody outsmart you out of your own money and start budgeting today by simply filling out the form below:

Want a free

ONE-AND-DONE CHECKLIST for aGUILT-FREE SPENDING PLAN? Free up your bandwidth and stop overthinking with this

FREE One-And-Done Checklist for your Guilt-Free Spending Plan!

Simply fill out the form below to get this strategy

delivered straight to your inbox!

How To Teach Yourself Intentional Spending & Financial Literacy

Intentional spending is the antidote to impulse spending. Instead of buying as a reaction, you start buying with precision. And let me be perfectly clear: this isn’t about cutting out all fun. It’s about deciding what resonates with you, then unapologetically ditching what doesn’t.

Pause & analyze the situation; you probably already know what lights you up in life. The problem is you haven’t mapped those joys onto your money yet. That’s why creating a list of life goals; whether it’s traveling, buying a home, or building your own business, is step one. Put numbers to those dreams. Suddenly, you have a map.

Next, set up a budget style that actually matches your wiring. If you’re intense and detail-driven, you’ll thrive on tracking. If you’re relaxed and hate spreadsheets, automate your bills and assign guilt-free spending money in a separate account. Intentional spending isn’t one-size-fits-all. It’s about making sure your system helps you, instead of drains you.

RELATED POST:

Intentional Spending: The CEO-Mindset And AntiDote Against Overspending & Impulse Buying

When you connect your money to goals that resonate with you, impulse spending stops feeling like a guilty high and starts looking like an obvious ‘no thanks.’ You’ll choose to invest in your future not out of pride, but out of the realization that you deserve better than to keep getting played by a consumer trap.

Turning Impulsivity Into A Strategic Rebellion

Impulse spending doesn’t vanish all of a sudden just because you decide to be intentional. But what it can do is transform into a signal. Every impulse is telling you something; about stress, boredom, or a craving for excitement.

Instead of scapegoating yourself, treat that impulse as data. Because you’re not fighting your impulses, you’re redirecting them. You’re saying, ‘Thanks for the info, brain, but let’s channel this energy into something that actually builds me.’

That might mean dopamine dosing with a small strategic reward after a week of sticking to your budget. Or it might mean creating a ‘temptation list’ where you write down the things you want, then revisit them in 30 days to see if they still resonate. Both approaches stop you from spiraling into self-blame and start turning your impulses into leverage.

What it truly is about is refusing to half-ass your life. You’re not rebelling against money. You’re rebelling against the idea that you’re too weak to handle it. And counterintuitively, when you take this rebel stance, your impulses lose their grip. Because now, instead of running from guilt, you’re running toward growth.

Impulse spending becomes less about a toxic loop and more about a powerful reminder: you’re meant for more than mindless consumerism. You’re meant for alignment, strategy, and the kind of life that marketing campaigns can’t sell you.

Impulse Spending (Summary)

Impulse spending often gets scapegoated as proof you’re weak, when the reality is a culture designed to tempt you everywhere you look. People confuse doing something bad with being bad, and that mix-up fuels shame instead of growth.

The tools that break you free are clear: step out of financial denial, map out life goals with real numbers, and choose a budgeting system that matches your wiring. Then, practice intentional spending, where you decide ahead of time what resonates with you, and redirect impulsive urges into strategic rewards instead of shame.

Picture this: instead of sinking in guilt every time you hit ‘buy now,’ you’ll feel like the CEO of your own life, aligned with your goals, and immune to cheap consumer traps. You’ll build momentum toward the life you’ve been craving instead of half-assing it.

I wish you the absolute best. Seriously. You’re not weak, you’re not flawed; you’re ready to rebel against staying small. Go grab life by the horns and make it yours. For what it’s worth, I believe in you!

This post was all about impulse spending, so you can stop scapegoating yourself and start reclaiming your future.

We aim to help you out as much as possible, but please keep in mind that the content is only for general informational and educational purposes. We offer our services based on independent research and life-experience only, and so our strategies can never serve as a substitute for professional advice. Trust me, we do not have 'everything figured out', are all still huge works in progress, but hey, what works for us, might work for you too! This is allll up for you to decide... It might not work for you, and that's okay, so cherrypick the stuff that resonates and leave the stuff that doesn't, and let's go!