Want to hear some budgeting money tips to make sure you do NOT break up with your budget? This post is all about the three most common reasons why people break away from their cashflow strategy, and what you can do to keep it going strong.

Cashflow strategies and budgeting can feel extremely depressing and demoralizing. I get it. If you’re in a love-hate relationship with your wallet, you’re definitely not alone. Preferring to avoid your income and expenses is unfortunately very common, but so are the reasons why!

You are going to learn the three most common reasons why people break up with their budget & some key budgeting money tips to prevent them from happening. Being able to prepare for the most common pitfalls will make it all MUCH easier.

After you’ve learned how to arm yourself against the common break-up patterns of budgeting you will be able to prevent cashflow failure, keep your strategy going strong and enjoy all the kick-ass confidence, self control & feelings of financial safety that it should have provided for you in the first place.

Here are some key budgeting money tips to prevent breakups with your budget so you can keep your cashflow strategy strong.

Budgeting Money Tips

Let’s be real: Keeping a cashflow strategy for your own personal use is hard emotional and mental work. The work itself and the concept are quite simple of course, but the practical side of it can be extremely stressful and dysregulating. Especially when the whole financial situation turns to shit again, all of us hear that little voice inside, whispering convincingly to just ignore the situation and focus on life itself.

Unfortunately, denial won’t get us out of those shitty situations, whereas being able to face the horrid consequences and acting accordingly most definitely will. But seriously, how do you pull yourself to a spreadsheet and handle the depressing view in front of you? We’re going to tackle all that pain of money management right here: Let’s start with spreadsheets themselves.

Budget Template

The concept of tracking your income and expenses in a spreadsheet is quite simple in itself. Unfortunately, the simplicity of the idea does not contribute to the chore itself being more ‘easy’ to do. Budgeting is HARD. It requires discipline, self-control, and especially emotional and mental strength. No matter how great the financial situation might be, or how used to budgeting you get, there will always be a boring component about doing the work.

One of the biggest favors you can do yourself (and your wallet), is to acknowledge that doing the actual work will not be fun. Set the right expectations! Don’t expect boring chores to automatically make you feel good. However, a positive mindset, a fancy budget sheet, and a clear goal can absolutely take the edge off the obnoxious components. What is it you achieve by tackling this task? What do you get out of it? I assume it’s because you’ll have full clarity about where you are financially & what is left to spend on fun things. Another thing that does wonders is to have a really fancy and aesthetic budget sheet going, one that would make you feel bad-ass and in charge of the situation as soon as you open it up. Instant dopamine rewards despite the boring chore! For me, budgeting is about responsibility, sanity and curiosity. I want to know, I want to track my progress and I want to get the most out of my income. This is the reward for the boring chore. And hey, if you’ve got the routine going, it’s usually just 15 minutes of upkeep. What’s 15 minutes a week if you get back confidence and peace of mind? Try to keep these rewards in mind when pulling yourself back to the sheet. Now let’s cover the three reasons why budget breakups happen:

Reason #1: Unsustainable Cashflow Strategy

Except for the fundamental requirement to spend less than you earn, controversially enough, there is not ‘one universal cashflow strategy‘ out there that’s a one-size-fits-all! Often people break up with their budget because they’re using a cashflow strategy that doesn’t align with their life and priorities. Not every method requires you to track every expense for example. If this is an extremely draining factor for you, you shouldn’t break up with budgeting, but instead consider another method! Make sure you choose a cashflow strategy that alignes with your personality & life-style. We’re going over some of the most common strategies and it’s pros & cons right here:

RELATED POST:

7 No-Bullshit Budgeting Strategies That Let You Spend Guilt-Free While Still Saving Big

When deciding which strategy to follow, keep in mind that it’s essential to be realistic about the time and discipline you can consistently put yourself through. If you have almost no bandwidth to deal with all this, why don’t you consider our Guilt-Free Spending Plan? This most likely is the quickest cashflow strategy out there! But first! Let’s look at some tips to shift the struggle into something sustainable:

- REDUCE THE NUMBER OF MONEY CHECK-INS

Daily budgeting is an extreme discipline that can drain you pretty darn fast, I would not recommend this to anybody. Instead, schedule a weekly money check-in, or at the start of the new money month. If your financial times are more turbulent, make sure to check in before bigger spending. Reflect on WHEN you really need the financial information to make good decisions and reduce the interval of check-ins according to those needs. - TRY A GUILT-FREE SPENDING PLAN (OR ANOTHER LOW-DISCIPLINE CASHFLOW STRATEGY)

Schedule ONE afternoon for opening up a bank account & looking over your income and expenses for the whole year. Determine how much you want to save, pay off debts, and pay bills. Set up automatic payments right after every payday so that it gets distributed accordingly. Then make another automated transfer, where the leftover of your income will be send to your newly opened bank account. You can now feel rest assured that everything has been taken care of. The money in the new account is yours to spend freely. - TAILOR A CASHFLOW STRATEGY TO YOUR OWN NEEDS

Pick one cashflow strategy that looks closest to your personal needs. Whereas the zero-based budgeting & ‘tracking your spending’ strategies require you to track where your every penny goes, the big cut strategy, reverse budget approach, bucket strategy & 50/20/30 method don’t require that much discipline and time. After having picked one, add things that you like from other methods or adjust the things that irritate you. The more you make it your own method, the higher the chance you won’t break up with it.

Owning a cashflow strategy is a skill that’ll give you some serious advantages in life. I think budgeting is an aligned action with taking life seriously, and I seriously believe life will reward you for it. If you’re not into high-maintenance strategies like ‘tracking your spending’ and just want to sit down ONCE to direct your financial future, our Guilt-Free Spending Plan Printable is the right cashflow strategy for you! Don’t let anybody outsmart you out of your own money and start budgeting today by simply filling out the form below:

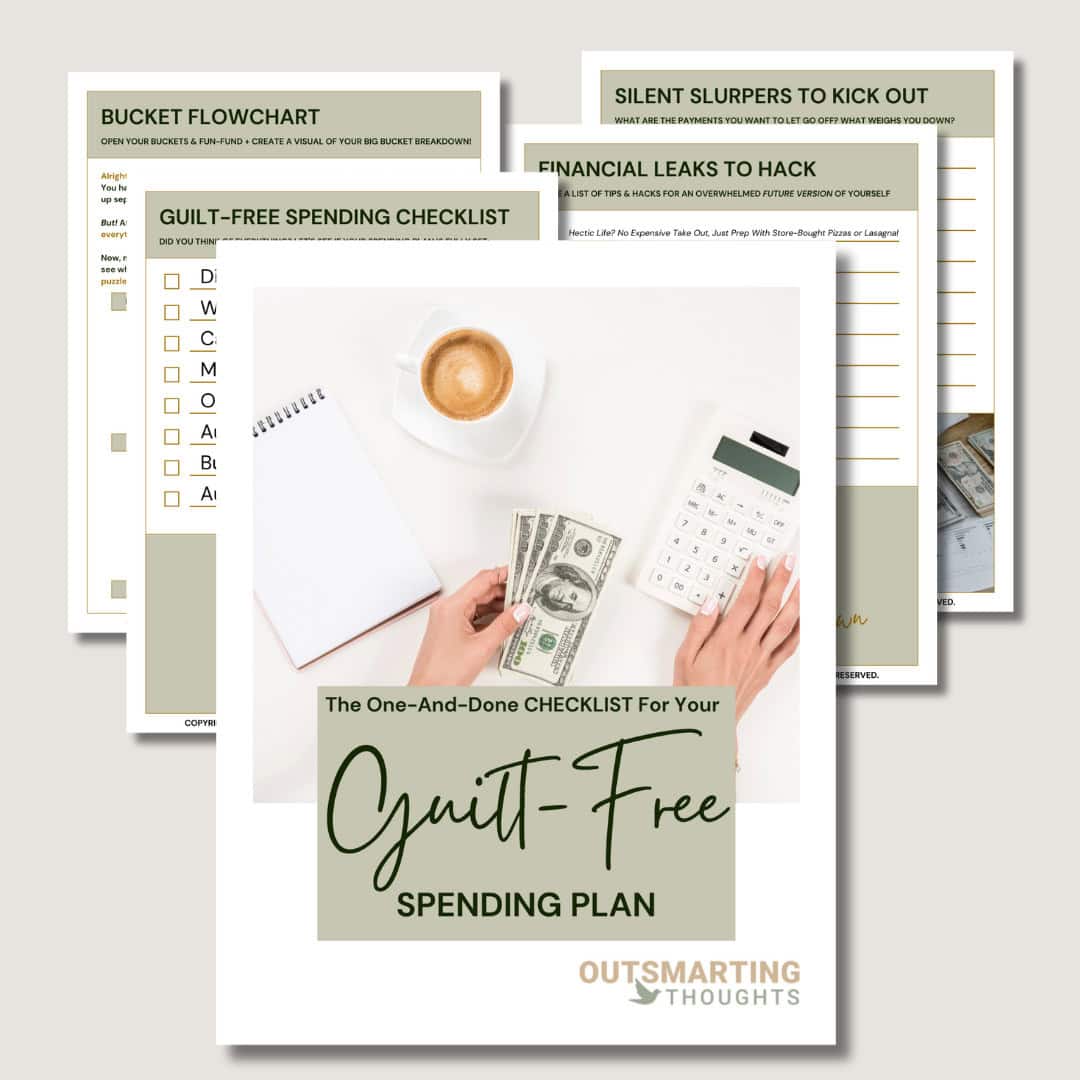

Want a free

ONE-AND-DONE CHECKLIST for aGUILT-FREE SPENDING PLAN? Free up your bandwidth and stop overthinking with this

FREE One-And-Done Checklist for your Guilt-Free Spending Plan!

Simply fill out the form below to get this strategy

delivered straight to your inbox!

Reason #2: Unexpected Bills Blow Up Your Budget

This is such a frustrating and derailing experience, I totally get it. I usually spend about an hour wanting to burn everything to the ground until I can finally come down to my senses again. Having a moment to be disappointed and wretched is still important to give yourself tho, there’s no way suppressing emotions will be good for your mental health. Just, whatever you do, do NOT ACT impulsively on negative feelings, and set a timer for your bad mood so it doesn’t end up ruining your whole day. And pretty please, with sugar on top: do not admit defeat after a big blow-up, and instead get back up and develop a counterattack with these tips:

- ADJUST INSTEAD OF ABANDON PLANS

Get back into your budget asap and reallocate the money you usually spend on non-essential categories like subscriptions or social spending for the time it’s necessary to cover the gap. Yes, it sucks hard, but you do need to make a sacrifice somewhere to cover the blow-up. By getting back into budgeting you can decide yourself which category has to bite the bullet. Pull the band-aid off and fix it as soon as you can. Having a recovery plan will make you feel less stressed and frustrated, and instead gives you back the feeling that you got this. - BUILD A BUFFER

Even keeping a small cushion can save your ass here. On good money months, withdraw extra cash, even if it’s only a 20 or a 50. Store it in some piggy bank or out-of-sight location at home for the typical rainy day and let it build up. Of course, you can also keep some in your bank account, but usually, that’s harder to do unless you have out-of-sight accounts already. I know it’s super old and worn-out advice to hide some cash in a sock, but it really helps with not giving up your cashflow strategy as soon as shit hits the van. - LEARN THE LESSON WITHOUT FEELING GUILTY

Nelson Mandela said ‘I never lose: I either win or learn’ and I still love this mantra. Instead of calling it quits, investigate the lesson that has to be learned here. Remember also that blame, shame & guilt will prevent you from learning any lesson. If you leave those three demons on mute: What can you learn from this setback? How can you be better prepared for the future? This leads us to the last tip for this break-up reason: - PLAN BETTER FOR IRREGULAR EXPENSES

Some expenses are feeling unexpected, while in reality, you KNEW they were coming up. What happened instead, was that you preferred to keep them out of sight until the deadline, because there was too much going on at the moment. Very common and understandable, again, don’t let guilt prevent you from learning the lesson! But birthday & Christmas gifts happen each year, and so does that ridiculously expensive dentist bill or the yearly car maintenance. If this is the reason why you keep breaking up with your budget, instead break up those big expenses into smaller payments so you have a standard expense each month. Makes the irregulars regulars. Saves you from blowing up unnecessarily too.

Reason #3: Budgeting Sucks Too Much Joy Out Of Life

Oh boy, I think we’ve all been here, haven’t we? How extremely valid! It sounds too funny not to laugh, but of course it’s extremely tragic when you think of it. This way of budgeting totally misses the point: Budgets and cashflow strategies shouldn’t feel as restricting as a straightjacket!? Again, maybe you would like to consider our Guilt-Free Spending Plan, so that you DO have a cashflow strategy, but only need to sit down once to be back in charge of your financial plan?

RELATED POST:

One-And-Done Checklist + Budgeting PDF: Unlock Guilt-Free Spending With This Simple & Fast Cashflow Strategy

In any case, budgeting is supposed to be your tool for freedom of choice and a gateway to getting what you want, not functioning as a dismissive soul sucker badgering you on until you’re ready to give up on existence. If this is your budgeting experience, then I hope these tips will help you reconsider getting back in the saddle:

- INCLUDE SOCIAL SPENDING & EXPERIENCES IN THE CASHFLOW STRATEGY

Budgeting should reflect your values, not cut out ALL the things you love. Even Ramit Sethy advised in his book I Will Teach You To Be Rich: ‘Spend extravagantly on the things you love, as long as you cut costs mercilessly on the things you don’t’, and this approach will feel unburdening compared to the straight jacket one. When you include social spending in your strategy, you can feel rest assured knowing you have money set aside for all the fun stuff. This really helps with preventing feelings of restriction and deprivation. You should feel empowered knowing you spend money on the things that are important to you. That’s absolutely NOTHING to feel guilty for or to cut out of your life. - AUTOMATE PAYMENTS AS MUCH AS YOU POSSIBLY CAN

I know this sounds super obvious, but I still have to mention it: automating bills, savings and debt payments will free up a LOT of your bandwidth. When you set up a direct transfer to your savings account right after payday, it reduces your mental load and at the same time, prevents the issue that you have no money left at the end of your money month. If budgeting feels too much to handle right now, you can also set up a 50/20/30 method when automating your bills, which will still make you have an above-average cashflow strategy! You should tailor your budget to YOUR needs instead of doing what you think you should do. - HAVE A REALISTIC SAVINGS RATE THAT ALLOWS YOU TO BREATHE

If you’re an overachiever like me, you might have unconsciously activated the ‘overdoing it cashflow strategy‘. I know it’s hard not to fall for, but do your ‘future overwhelmed self’ a favor and focus on good enough instead of perfect. Your financial situation is not going to hell when you overspend occasionally or forget to track for a while, nor will an insane high savings rate make your present-day life any more pleasurable or comfortable. Do not sacrifice your life right now for sights in the future, or at least, not in extreme forms. Instead, be fair to yourself in the moment while preparing for future fun. - REWARD YOURSELF FOR STICKING TO MONTHLY STRATEGIES & SAVINGS MILESTONES

I know, I know, you’re already thinking, then I have to budget this in too? Hah, well, YAH. But it doesn’t have to be major! In fact, it shouldn’t. Just treat yourself to a small splurge: the normally too expensive coffee, a new book or your favourite meal are already very good targets. Rewards have the amazing natural consequence that they create positive habits, so it’s kinda like you’re investing in your healthy habits. See it as upkeep costs. If you could pay 10-20 bucks for feeling good about your money ALL month, wouldn’t you spend it right away?

Budgeting Money Tips (Summary)

If you want to prevent a breakup with your budget, you need to make sure that your cashflow strategy actually aligns with your personality & lifestyle. If you then also include the preparation of unexpected budget blow-ups by thinking even further ahead, and making sure you’re working towards goals so that the obnoxious chore of budgeting is at least ‘worth it’ , then you’re so well prepared, I would place my bets on you 😉

I wish you all the mental strength required to keep your strategy going strong and hope you’ll enjoy all the kick-ass confidence, self-control & feelings of financial safety that it should have provided for you in the first place.

This post was all about key budgeting money tips so you can keep your cashflow strategy strong

We aim to help you out as much as possible, but please keep in mind that the content is only for general informational and educational purposes. We offer our services based on independent research and life-experience only, and so our strategies can never serve as a substitute for professional advice. Trust me, we do not have 'everything figured out', are all still huge works in progress, but hey, what works for us, might work for you too! This is allll up for you to decide... It might not work for you, and that's okay, so cherrypick the stuff that resonates and leave the stuff that doesn't, and let's go!